Merchant Cash Advance — How IBM & Verifone met Barbara Johnson's Invention

I would firstly like to apologise for not posting the newsletter last week, I was travelling and consequently did not have time to edit.

Cool.

This week I want to dive into Merchant Cash Advance (MCA) & what alternative MCA lenders exist for small businesses in South Africa. To start, what is Merchant Cash Advance (MCA)? MCA is a form of a business loan where the merchant (small business) sells a percentage of their future debit & credit transactions in exchange for an upfront lump sum.

MCA began in the 1990s with Barbara Johnson but to really understand it we need to go back to the core — the first store of value, the credit card, the magnetic strip & the barcode before that.

“Barbara Johnson was running four Gymboree Playgroup & Music franchises. Unable to get working capital to fund a summer marketing campaign, she wondered whether she could borrow against future credit card sales from parents bringing their kids back for fall classes” - Kevin Voigt, Staff writer @Nerdwallet

IBM, one of the most innovative companies of the 20th century had a series of inventions during the 50s, 60s & 70s. Norman Joseph Woodland and Bernard Silver patented the barcode in 1951. In the same year, Woodland went to work for IBM & pressed them to look into the technology for almost a decade. IBM found the research compelling and feasible but the use case for a bulls-eye printing pattern would require resources & equipment that have not been developed yet. Years went past, then in 1962 IBM offered to buy Woodlands patent but he rejected & sold it to Philco which they then sold to RCA. In 1966 the National Association of Food Chains (NAFC) had a council meeting where they concluded the need for an automated checkout system at the point of sale. RCA was part of that meeting & commissioned a project to create a barcode scanning system based on the bulls-eye pattern on Woodland’s & Silver’s patent, which RCA owned. RCA then sent out a tender for the development of what was to become the Universal Product Code (UPC) to a variety of companies — including IBM. IBM saw what RCA was trying to do with the technology they used to control but could not find any viable use case for it until now. IBM knew that the bulls-eye pattern was not going to work so they developed their own barcode using a linear approach. In 1973 IBM released the linear Universal Product Code (UPC) to the NAFC. It would take time for the UPC to be adopted but by 1980s the UPC-A barcode was used by most supermarkets including by the US government. Supermarket chains became pioneers of the modern-day point of sale system because of the IBM 3650 & 3660 terminals.

In 1959 American Express released the first plastic credit card, before that credit cards were made from cardboard. Then in 1960, IBM started to develop a way to encode the digital data stored on the magnetic tape & securely place a magnetic strip onto the plastic credit card. IBM spent the whole decade trying to do this. In 1969, an IBM engineer by the name of Forest Perry with the help of his wife (Mrs Perry) found a way to securely place the stripe onto the card by melting it. Banks, Insurance companies, governments & hospitals started to supply IBM with plastic cards so they could place magnetic strips & encode data on them. By the end of the 70s IBM’s technology was the bedrock for storing valuing & transmitting data at the point of sale.

Credit cards went global in the 1970s with the rise of Visa & Mastercard but money was not really digital. The magnetic strip made it digital. In 1979 Visa released a set of electronic point of sale terminals (card machines) but it would be Verifone that would revolutionize them.

Bill Melton founded Verifone in 1981. Verifone, which stands for Verification Telephone is a multinational organisation focused on electronic point of sale terminals & other merchant facing value-added services. In the 70s, Visa & Mastercard were losing millions of dollars in processing fees due to credit card fraud & needed a way to securely authenticate payments. In 1983 Verifone released the ZON JR XL. The ZON JR XL was smaller & cheaper than the other devices that were in the market. At the time the average price of a card machine was $900 — the ZON JR came to market at $500. Verifone was disruptive, gaining a 50% market share of all point of sale terminals in the US. By 1993 Verifone was in 70 countries & shipped its 3 millionth device.

Verifone ZON JR XL

Verifone VX 820

In the 1990s when Barbara Johnson was looking for a loan for her business & thought of borrowing against her future sales — she believed more people were in the same predicament. So, Barbara & her husband Gary Johnson created a company called AdvanceMe in 1997. AdvanceMe is the first Merchant Cash Advance (MCA) company. What AdvanceMe did was to patent a technology that lets the lender split a portion of a credit or debit transaction as a way to repay a loan.

Barbara S Johnson Patent

How Barbara Johnson’s split-funding MCA works:

“After a customer identifier (e.g., a credit, debit, smart, charge, payment, etc. card account number) is accepted as payment from the customer, information related to the payment is forwarded to a merchant processor. The merchant processor acquires the information related to the payment, processes that information, and forwards at least a portion of the payment to a loan repayment receiver as repayment of at least a portion of the outstanding loan amount owed by the merchant. The loan repayment receiver receives the portion of the payment forwarded by the merchant processor and applies that portion to the outstanding loan amount owed by the merchant to reduce that outstanding loan amount”

In English: How it worked in 1999.

The MCA lender uses a B2B2B model where they integrate their technology onto the point of sale terminals (card machines) & processor.

The Merchant (small business) needs capital (R80 000) to grow their business, no bank wants to give them a loan so they approach the MCA lender who gives them a lump of (R80 000) in exchange for future transactions on their card machine to the amount of R100 000 (agreed percentage = 20%).

A customer walks into the shop, to buy an item (R1000). The merchant scans it (barcode), the customer then swipes* their card (magnetic stripe) on the card machine (Verifone). The R1000 is then reserved for purchase (Visa or Mastercard) & upon settlement, the processor will give the merchant R800 & the MCA lender R200. This will be done until the R100 000 is settled.

The more transactions a merchant has, the quicker they can pay off the loan.

*Today people dip cards into a machine or utilize tap & pay. Chips are more secure than magnetic stripes.

Over the last decade, there has been an increasing adoption of card machines in South Africa amongst small businesses. With that meant an increasing need for working capital and in turn, gave rise to MCA lenders:

Retail Capital (raised $40 million in 2019)

Merchant Capital (raised > R25 million in 2015)

Lulalend (raised $6.5 million in 2019)

Growise Capital (new to the market)

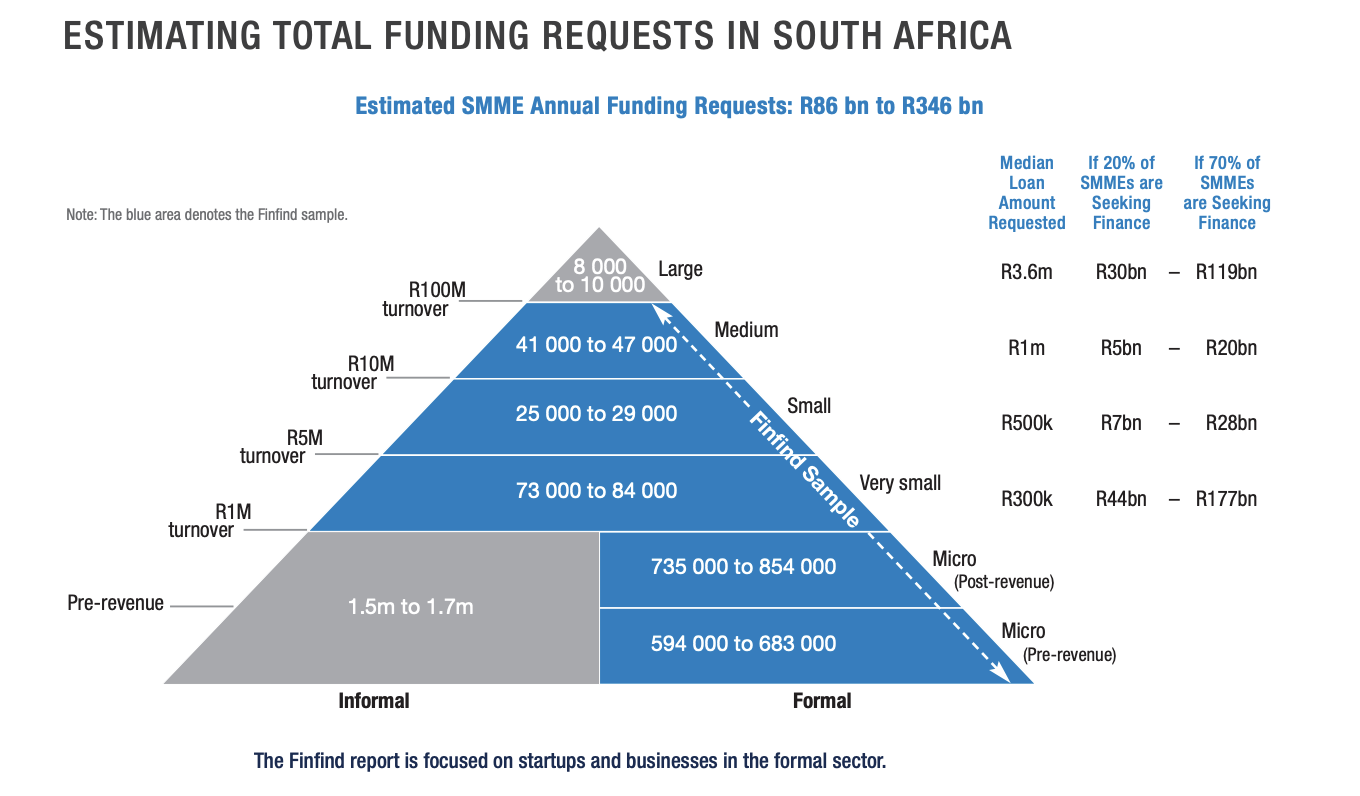

In their 2018 SMME report, FinFind shared that SMMEs require up to R346 billion in funding.

“According to the FinScope (2010) study, 13% of formal businesses had accessed funding and 7% of businesses do not borrow because they don’t qualify” - INAUGURAL SOUTH AFRICAN SMME ACCESS TO FINANCE REPORT by FinFind

It cannot be echoed enough that small businesses in South Africa need capital assistance. MCA has helped a lot of small businesses in but if they aren’t transacting they cannot pay back the loan.

MCA has its limitations, distribution being one of them. This is why the same MCA players in the market are finding other ways to reach customers using technology & alternative ways to underwrite small businesses. Then there’s the grey area they operate in. Currently, there’s no regulatory body that governs these new alternative lenders besides the National Credit Regulator, who by some measure does not do enough to protect small businesses against predatory lending. These new players have chosen to self regulate via their own industry body, the South African SME Finance Association (SASFA). One can argue that in South Africa we love governing bodies just as much as we love pyramid schemes but in this case, it is necessary. As long as small businesses have access to the tools they need to grow we should all support & encourage innovation in the alternative lending sector.

Technology has always been the connecting factor of modern society. The idea that small, seemingly uncorrelated inventions in the 60s & 70s can have compounding effects years later isn’t unimaginative. MCA is an old technology but has found new life in South Africa thanks in part to the proliferation of technology made by IBM & the inventions of both Bill Melton & Barbara Johnson.

Take care.